II. Depreciation Expense

When a business buys an asset it in effect buys a “fund of usefulness”. Day by

day as the asset is used in the operations of the business, a portion of this usefulness is

consumed or expired. In accounting, this expiration of an asset’s usefulness is called

depreciation. All fixed assets except land lose their usefulness. Decreases in the

usefulness of assets that are used in generating revenue are recorded as expenses.

Depreciation is an expense and is deducted each year until the cost of the asset is

expensed. The account debited is a depreciation expense account. The account credited

is an accumulated depreciation account. Accumulated depreciation accounts are called

contra accounts because they are deducted from the related asset accounts on the balance

sheet. The use of a contra account allows the original cost to remain unchanged in the

fixed asset account. Depreciation is called a non-cash expense since no actual dollars

exchange hands. There are several methods of calculating depreciation with the most

common being straight line.

Depreciation Expense example:

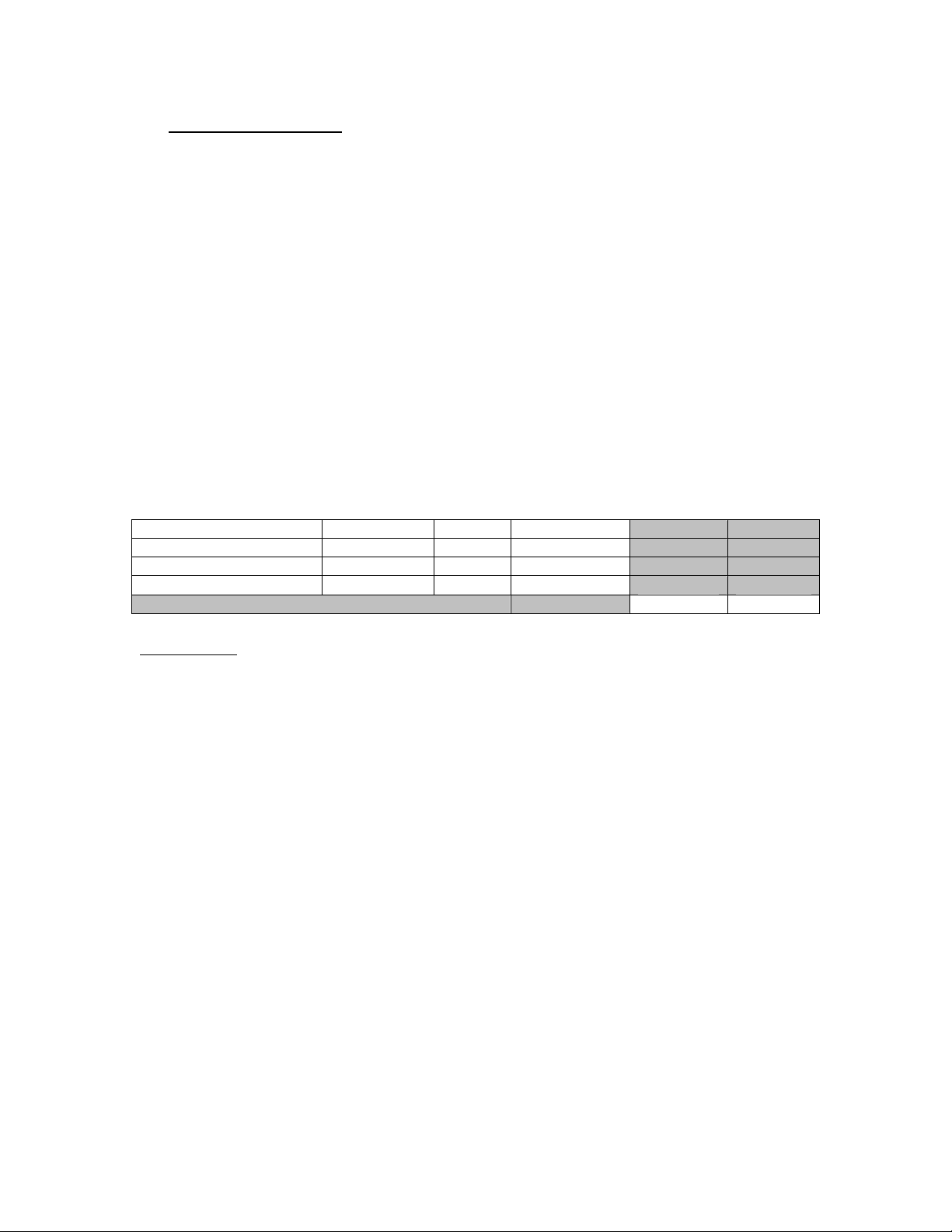

a. An accountant figured the depreciation for a business as follows: equipment

depreciation of $2500 and improvement depreciation of $1500.

Account Name/Number Account type Increase Decrease Debit Credit

Depreciation expense Expense 4,000 4,000

Accum Depreciation Equip Asset 2,500 2,500

Accum Depreciation Impr. Asset 1,00 1,500

Totals 4.000 4,000

Explanation: Depreciation is an expense that affects the income statement by lowering

the net income. This expense increases by $4,000 the total of the depreciation for the

equipment and the improvements. It can be entered into more than one depreciation

account depending on your preference. The dollar amounts in the accumulated

depreciation account decrease each year as the life of the asset is used up. Depending on

the set-up, there could be a separate depreciation account for each depreciable asset such

as equipment and improvements.