© 2010 The McGraw-Hill Companies, Inc.

Standard Costs and Operating

Performance Measures

Chapter 11

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

Chapter 11 powerpoint notes Material Type: Notes; Class: Managerial Accounting; Subject: Accounting; University: Pittsburg State University; Term: Forever 1989;

Typology: Study notes

1 / 70

This page cannot be seen from the preview

Don't miss anything!

© 2010 The McGraw-Hill Companies, Inc.

Chapter 11

Quantity standards specify how much of an input should be used to make a product or provide a service. Price standards specify how much should be paid for each unit of the input.

Prepare standard Prepare standard cost performance cost performance report report Analyze variances Begin Identify questions Receive explanations Take corrective actions Conduct next period’s operations

Explain how direct Explain how direct materials standards materials standards and direct labor and direct labor standards are set. standards are set.

Summarized in a Bill of Materials. Final, delivered cost of materials, net of discounts.

Often a single rate is used that reflects the mix of wages earned.

Use time and motion studies for each labor operation.

The rate is the variable portion of the predetermined overhead rate.

The quantity is the activity in the allocation base for predetermined overhead.

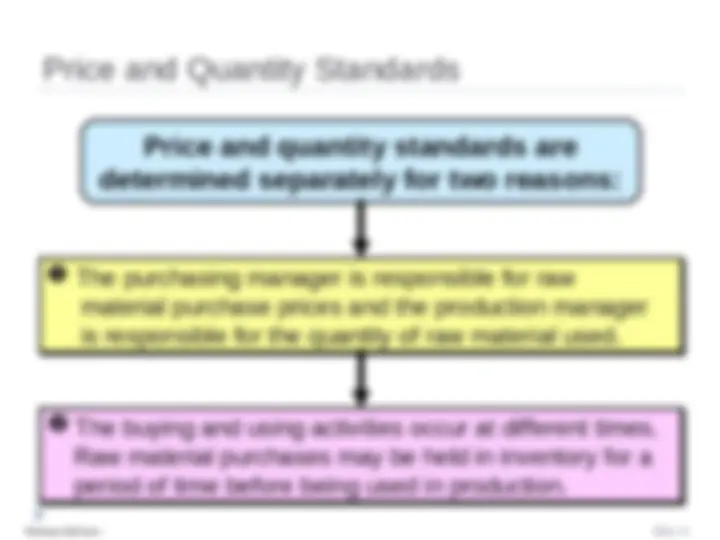

(^) The purchasing manager is responsible for raw material purchase prices and the production manager is responsible for the quantity of raw material used. (^) The purchasing manager is responsible for raw material purchase prices and the production manager is responsible for the quantity of raw material used. (^) The buying and using activities occur at different times. Raw material purchases may be held in inventory for a period of time before being used in production. (^) The buying and using activities occur at different times. Raw material purchases may be held in inventory for a period of time before being used in production.

Difference between Difference between actual price and actual price and standard price standard price

Difference between Difference between actual quantity and actual quantity and standard quantity standard quantity

Actual Quantity Actual Quantity Standard Quantity × × × Actual Price Standard Price Standard Price

Actual Quantity Actual Quantity Standard Quantity × × × Actual Price Standard Price Standard Price

Actual Quantity Actual Quantity Standard Quantity × × × Actual Price Standard Price Standard Price

Actual Quantity Actual Quantity Standard Quantity × × × Actual Price Standard Price Standard Price